What is home title theft (deed fraud)? How to spot it and protect your home

Home title theft, also known as deed fraud (or title fraud), is a scam in which someone files fraudulent property documents to make it appear that they own the property.

It often doesn’t require moving into the home. Instead, it exploits the fact that property ownership information is recorded in public systems and that a recorded document can create serious legal and financial problems even if the transfer is ultimately invalid.

This guide explains how home title theft occurs, who’s most at risk, and how to protect yourself.

Please note: This information is for general educational purposes and not financial or legal advice.

How does home title theft work?

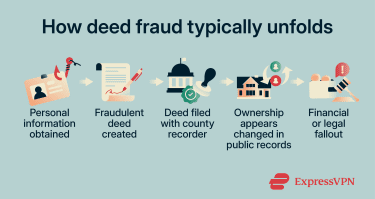

Deed fraud happens when someone submits paperwork that appears legitimate to change public records about a property’s ownership. That can “cloud” the title, creating confusion for buyers, lenders, and title/closing professionals and sometimes delaying a sale or refinancing until the record is corrected.

This typically starts with one of two tactics. The first is forgery, where a fraudster files a deed with a forged signature (including forged quitclaim deeds). The second involves deception, where the homeowner is tricked or persuaded (often during financial distress scams) to sign over the deed/ownership, sometimes under the claim that it's temporary or part of a rescue arrangement.

In both cases, the fraudster aims to get the document recorded with the local recording authority (such as a county clerk or recorder). Recording offices generally review documents for compliance with filing requirements. They typically do not conduct full investigations into the underlying transaction at the time of recording.

Identity theft can also be part of deed fraud, with criminals using stolen personal information (and sometimes fake identification) to impersonate an owner during signing or notarization. This doesn’t make the transfer “legitimate,” but it can make the dispute longer and more complex to unwind.

A fraudulent filing can sit on record without obvious alerts (unless a jurisdiction offers recording notifications), so it’s often discovered only after an unexpected notice, a title search, or an attempt to sell or refinance

A forged deed can also sit in official records without triggering any alerts. Most homeowners only discover the problem when an unexpected notice arrives or a routine record check flags a filing they never authorized.

It’s worth noting that deed fraud differs from mortgage fraud. Mortgage fraud involves false information to obtain or fund a mortgage loan, while deed fraud centers on the (fraudulent) transfer of ownership.

Read more: How to find out if someone is using your identity.

What can criminals do with a home title?

Once a fraudster creates the appearance of ownership, they can use that false record to exploit the property in several ways:

- Borrow against the property: The scammer may try to take out a mortgage or other loan using the property as collateral.

- Attempt to sell the home: Another common play is to “sell” the property to an unsuspecting buyer and take the proceeds. Even if the transfer is ultimately invalid, it can leave the buyer without a legitimate claim and force the true owner into legal proceedings to clear the title.

- Collect rent or attempt eviction: In some cases, scammers pose as the legitimate owner to collect rent from tenants, or they may attempt to start eviction proceedings.

How common is deed fraud?

Deed fraud is difficult to isolate in the FBI’s Internet Crime Complaint Center (IC3) data because IC3 does not publish separate statistics for title fraud; it is included under the broader real estate crime category.

What is available suggests that real estate fraud causes significant financial harm. From 2019 through 2023, IC3 received reports from 58,141 U.S. victims, totaling $1.3 billion in losses related to real estate fraud nationwide; deed fraud is included within those totals rather than listed separately.

The real number is likely higher. Many victims don't know where to report fraud, feel embarrassed, or haven't yet realized they were targeted. That gap is especially relevant to deed fraud, since the problem may not surface until someone tries to sell, refinance, or transfer the property. Local recording offices may also play a role in surfacing suspicious filings (and some offer title alert options), but detection can occur at multiple points in the process.

Deed fraud isn't limited to the U.S. In England and Wales, HM Land Registry reports that in 2024 to 2025, it received 4,429,092 applications to create or update the Land Register and identified 86 as fraudulent.

Who is most at risk?

Fraudsters typically look for properties that are easier to transfer on paper or less likely to be closely monitored. This means the risk is higher for:

- Owners with paid-off homes: Properties without a mortgage (sometimes called “unencumbered” properties) can be more attractive targets, and some research finds deed fraud often targets unencumbered properties, especially when they’re also vacant.

- Older or vulnerable owners: Some reports suggest that older adults and homeowners experiencing financial distress have been disproportionately targeted by deed fraud schemes. Fraudsters may use forged signatures or trick individuals into signing documents they don’t fully understand.

- Landlords and absentee owners: Properties that are rented out, empty, or owned by someone who doesn’t live there (including living overseas) can be higher risk because suspicious filings or mail may be noticed later.

- Homeowners in default or facing foreclosure: Fraudsters may target homeowners with misleading "rescue" offers that pressure them into signing over the deed, believing they're getting help rather than transferring ownership.

Being in one of these categories doesn’t mean fraud is inevitable. That said, it warrants vigilance regarding recorded documents, unexpected mail, and unusual real estate activity.

Signs your home title may be at risk

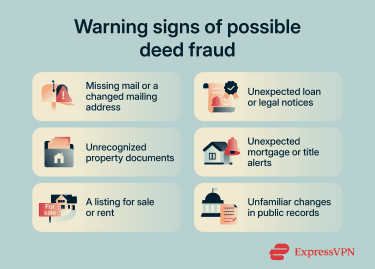

Deed fraud rarely announces itself. In many cases, the first clue is something small that doesn't add up. Common warning signs include:

- Missing mail or a changed mailing address: Property tax bills, utility notices, or other official mail suddenly stop arriving, or the mailing address connected to your property records changes without authorization.

- Unexpected documents or notices: A loan statement, lien notice, legal filing, or recorded document tied to the property that was never authorized.

- Mortgage or title alerts: A title monitoring service notifies you that a deed or document has been recorded against the property that you didn't authorize.

- Sale or rent listings: The property is advertised online for sale or rent without the legitimate owner's involvement.

- Unfamiliar changes in public property records: Ownership information, deed history, or recorded documents change without your approval.

Early detection can help limit damage and may speed up resolution, especially if suspicious filings are flagged quickly.

Read more: Online address change scam.

How to protect yourself from deed fraud

You can make your home a harder target by monitoring property records, protecting personal information, and handling ownership documents carefully.

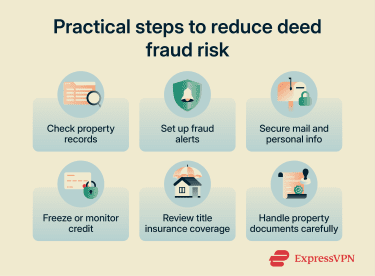

Check your property records regularly

Start with a simple habit: look up your property record every so often through your county recorder or clerk’s office. Confirm that basic details like the owner’s name, mailing address, and recently recorded documents match reality.

A quick check is especially useful after major changes involving the property, such as ownership, occupancy, or important paperwork. If something looks unfamiliar, download a copy of the record to compare changes over time.

In addition to manual checks, monitoring can help flag changes sooner. Certain tools, like ExpressVPN ID Alerts (available to U.S. users on select ExpressVPN subscriptions), can help monitor for identity-related signals that may overlap with deed fraud risk, such as change-of-address activity, court records, and high-risk transactions.

Set up county recorder fraud alerts

Check whether your county offers fraud alert programs that notify you when documents are recorded under your name. Some programs may ask for variations of a name (for example, with and without a middle initial) so alerts match more filings.

Keep in mind that alerts are an early warning system, not a prevention tool, so treat any unexpected notification as urgent until it's verified.

Protect your mail and personal information

Many real estate scams rely on obtaining personal details. You can reduce your exposure by adopting a few habits:

- Shred sensitive documents: Don’t simply bin tax documents, mortgage statements, insurance letters, and any mail that contains account numbers or personal details.

- Be cautious with unexpected property services: If a letter says you need to pay to secure your deed, update your title, or fix your records, verify it before acting. Many legitimate recorder services are free or low-cost, and your county website will clarify what is official.

- Use official channels for address changes: If you’re changing your mailing address, use the official Postal Service process (for example, via usps.com). Bogus or look-alike change-of-address sites exist, and the Postal Service has warned about them.

- Limit what you share publicly: Avoid posting your full address, phone number, or other personal details on social media, online directories, or community forums.

- Consider a data removal service: Data broker sites can list personal details such as addresses and phone numbers. A data removal service can help reduce exposure by requesting removals from these listings.

These steps don’t eliminate risk entirely, but they reduce the amount of information tied to your name.

Monitor your credit and freeze it when appropriate

A credit freeze won’t stop someone from recording a fraudulent deed, but it can help prevent the damage from spreading into new credit accounts opened in your name.

If you’ve experienced a data exposure, spotted suspicious mail, or noticed questionable activity tied to your property, freezing your credit is a practical defensive step. In the U.S., it's free, stays in place until you lift it, and you can temporarily remove it when applying for credit.

Credit monitoring can add another layer by alerting you to changes that may signal identity-based fraud (such as new accounts, hard inquiries, or other activity tied to your credit file).

Understand what title insurance does and doesn’t cover

Title insurance protects against certain title defects, typically those that existed before you purchased the property. Coverage depends on the policy and the timing of the issue.

If you're concerned about post-purchase deed fraud, contact your title insurer and ask what your policy covers, whether there are exclusions related to fraud, whether fraud-related exclusions apply, and whether endorsements are available in the state.

Be careful with notarizations and document sharing

Notarization reduces fraud risk by confirming a signer’s identity, but it doesn’t replace diligence or guarantee a document is legitimate. When handling any property-related paperwork:

- Don’t sign what you don’t understand: If you feel rushed, stop. A legitimate transaction can wait for your review.

- Treat deed-related paperwork as high risk: If someone asks you to sign a deed, quitclaim deed, power of attorney, or ownership transfer document outside a normal closing process, verify it independently.

- Share IDs and personal documents only when truly required: If a copy of your ID is requested, ask why they need it, how they will store it, and who will have access to it.

- Be wary of informal shortcuts: Legitimate property transactions follow a process. If something feels unusually casual or rushed, slow down and verify independently.

What to do if deed fraud happens to you

If you discover a suspicious deed or property filing, act quickly but stay methodical.

- Confirm the filing with the county recorder: Contact your county recorder or clerk's office and request certified copies of the document in question (and a certified copy if needed/available). Verify exactly what was recorded before taking further steps.

- Report it and document your evidence: File a police report and, if the fraud involved online activity, report it through the FBI’s IC3. Also, consider filing an identity theft report through the Federal Trade Commission (FTC) if personal information was used. Keep copies of all documents, notices, envelopes, screenshots, and correspondence tied to the suspicious filing.

- Notify your title insurer, lender, and credit bureaus: If there's owner's title insurance, contact your insurer to understand what your policy covers. If the property has a mortgage, notify your lender. Consider placing a fraud alert or credit freeze with the major credit bureaus to reduce the risk of further identity-based fraud.

- Work with an attorney to clear the title: Removing a fraudulent deed from the record can require legal action. Recording offices generally record documents but typically don’t determine whether they’re valid, so an attorney may need to pursue a court order to correct the record or “quiet” the title. Laws and procedures vary by jurisdiction.

Once the immediate issue is addressed, keep monitoring your property record for new filings.

FAQ: Common questions about home title theft

Can someone steal my house without my knowledge?

How do I know if my deed was changed?

Does title insurance cover deed fraud?

Should I freeze my credit to prevent deed fraud?

What if my property is in default or foreclosure?

How long does it take to fix deed fraud?

Where do I report deed fraud?

Take the first step to protect yourself online. Try ExpressVPN risk-free.

Get ExpressVPN