Is Zelle safe? What to know before you send money

Zelle is a peer-to-peer payment service built into many US banking apps. Because it’s integrated with your bank, using it can feel as secure as any other financial activity. But how safe is it in practice?

Zelle is secure by design, but your safety depends on how you use it. Transfers are fast and irreversible, which means mistakes and scams are harder to fix than with other payment methods.

This guide explains how Zelle’s security works and practical ways to reduce risk. It also covers what to do if money is sent to the wrong person.

How does Zelle work?

Zelle lets you send and receive money directly between bank accounts through participating banks and credit unions.

Instead of entering full bank details, money can be sent using just an email address or phone number. This makes everyday payments easier and means recipients don’t see sensitive financial information.

Unlike standard bank transfers, Zelle moves money quickly, often within minutes. Sending money is typically free. It’s useful for splitting bills or paying someone you know within the U.S.

Who can use Zelle?

Zelle is available through many U.S. banks and credit unions. To send or receive money, both the sender and recipient need eligible U.S. checking or savings accounts. It doesn’t support international transfers.

To get started, you simply enroll your email address or mobile number. That contact detail becomes your Zelle ID, which other people use to send money to you.

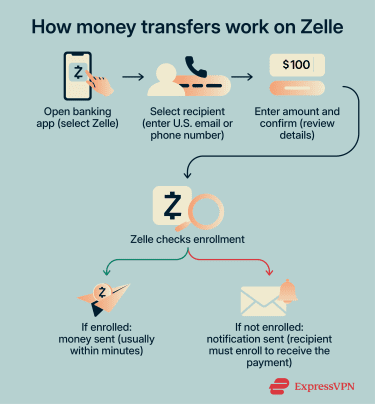

How money transfers work on Zelle

When you send money through Zelle, the funds move directly between bank accounts using your existing banking network. Here's how a standard transfer works:

- You open your banking app and select Zelle.

- You choose a recipient from your contacts or enter their email or US phone number.

- You enter the amount and confirm the payment.

- Zelle looks up the recipient to check whether they're enrolled in Zelle. If they are, the money typically arrives shortly after.

- If the recipient isn't enrolled, Zelle sends them a notification with instructions to sign up. The payment is held until they enroll, or it's canceled after a set period.

Once sent, payments are immediate and final. Zelle treats transfers like cash and doesn’t offer built-in buyer or fraud protection, so there’s no option to cancel a transaction once the recipient has received the funds. Because of this, it's important to verify you're sending money to the right person before confirming any payment.

Once sent, payments are immediate and final. Zelle treats transfers like cash and doesn’t offer built-in buyer or fraud protection, so there’s no option to cancel a transaction once the recipient has received the funds. Because of this, it's important to verify you're sending money to the right person before confirming any payment.

Why payments move so quickly

Most Zelle payments arrive within minutes, which is possible because the platform operates within the existing banking network rather than routing money through a third-party wallet or processing system.

When you send money, Zelle communicates directly with both banks involved to authorize and complete the transfer. There's no holding period, and no funds sit in an intermediate account. The money moves from your account to the recipient's account almost instantly.

Understanding Zelle’s safety features

Zelle includes several safety features designed to protect your data, verify your identity, and monitor transactions. However, these protections have limits, especially in situations where you authorize a payment yourself. Here’s a closer look at how Zelle helps keep your information and transactions secure.

Built-in security through your bank

Because Zelle is integrated directly into your bank's app, it inherits your bank's existing security framework. That includes fraud monitoring systems that flag unusual account activity, transfer limits, account lockout protocols if suspicious behavior is detected, and secure login requirements set by your financial institution.

How Zelle protects your information

Zelle uses your bank’s encryption to protect your data as it moves between your device and the payment network. This means your personal and financial information is scrambled during transmission, making it difficult for unauthorized parties to access.

Zelle also uses your bank’s authentication measures to verify your identity when you log in or make a payment. Depending on your bank, this might include multi-factor authentication (MFA), one-time passcodes, or biometric verification such as fingerprint or face ID.

Is Zelle safe to use?

Zelle is generally considered safe when used to send money to people you know and trust. However, Zelle doesn’t offer built-in buyer protection for authorized payments.

When Zelle is safe

Common use cases where Zelle is generally safe include:

- Splitting costs with friends or family, such as shared bills, meals, or travel expenses.

- Paying people you know personally, such as a roommate who covered a shared expense.

- Paying a landlord or service provider you have an established relationship with, where the arrangement is clear and agreed upon in advance.

In these cases, the risk of fraud is lower because you already know and trust the recipient.

When Zelle can be risky

Zelle typically carries more risk in situations involving strangers or unverified recipients. For example:

- Paying strangers for goods or services, such as items listed on Facebook Marketplace or similar platforms. Zelle has no buyer protection, so if an item never arrives or doesn't match its description, there's no mechanism to recover the funds through Zelle.

- Responding to unsolicited payment requests, particularly from people or organizations you weren't expecting to hear from.

- Sending money under pressure or urgency, such as when someone claims there's a time-sensitive reason you need to act immediately.

- Paying for rental deposits or large transactions with someone you've only met online, where you haven't been able to verify the other party's identity.

- Using Zelle through a link or prompt sent via text or email, rather than through your bank's official app.

To reduce risk, only use Zelle to send money to people you know and trust, and avoid using it for purchases, deposits, or payments where you may need to dispute the transaction later.

Common risks of using Zelle

Many of the risks associated with Zelle come from malicious actors who exploit its speed and convenience to deceive users into sending money.

Common risks include being tricked by an impersonator, sending money for something that never arrives, or responding to a fake payment request or refund message. In other cases, criminals may try to access a victim’s bank account using stolen credentials and then use Zelle to move funds quickly.

If a stranger, seller, supposed bank representative, or online contact asks you to pay with Zelle, treat that as a warning sign and verify the situation independently before taking any action.

Read more: For a closer look at the most common schemes, see our guide to Zelle scams.

How to use Zelle safely

Zelle can be a safe way to send money when you follow a few basic precautions.

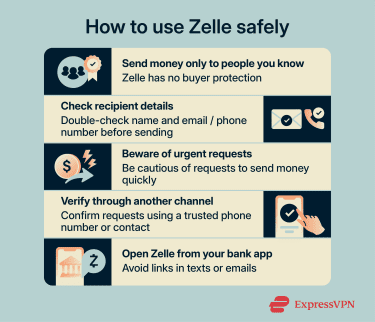

Only send money to people you trust

Zelle doesn't offer a dispute resolution process, so the primary safeguard is your own judgment about who you're paying. As a general rule, limit Zelle payments to people you know personally, such as friends, family, or established contacts. For transactions with strangers, such as buying items through online marketplaces, opt for payment methods that include buyer protection.

Verify recipient details before sending

Before you send a payment, double-check the recipient’s information. Zelle transfers are usually linked to an email address or phone number, so even a small mistake can send money to the wrong person:

- Double-check the email address or phone number you've entered against a known, trusted source, not a number or address sent to you in the same conversation where the payment was requested.

- Contact the recipient through a separate channel to confirm their details if you're paying someone for the first time.

- Confirm the recipient's name as it appears in the Zelle confirmation screen before completing the transfer.

- Confirm that the amount is correct and reflects what was agreed and that the payment purpose is clear.

These steps take only a few seconds but significantly reduce the risk of sending money to the wrong person.

Watch for urgent or unusual requests

Scammers often try to create a sense of urgency to make you act quickly. Messages that ask you to send money right away, especially for unexpected reasons, should be treated with caution.

Be careful if someone:

- Claims there’s an emergency.

- Says your account is at risk and you must act now.

- Asks you to send money to fix a problem.

- Pressures you to complete a payment quickly.

The same applies to unusual payment scenarios, such as being asked to send money to someone you don't recognize or being told to use Zelle specifically when another payment method would be equally convenient.

Use your bank app

Always access Zelle through your bank's official mobile app. Avoid opening links in text messages or emails that claim to direct you to Zelle or your bank, even if the message appears to come from a familiar source.

Fraudulent links can lead to spoofed websites designed to capture your login credentials for account takeovers. If you receive a text or email prompting you to take action on your Zelle account, go directly to your bank's app instead.

What to do if you sent money to the wrong person or a scammer

While recovering money sent on Zelle isn’t guaranteed, acting quickly can improve the chances of resolving the issue. If you realize that you sent money to the wrong person or responded to a scam, here’s what you should do.

Contact your bank right away

If you think you sent money to the wrong person or were tricked into making a payment, the first step is to contact your bank or credit union immediately. The sooner you report the problem, the more options your bank may have to review the transaction.

When you contact your bank, be ready to provide:

- The date and amount of the payment

- The email address or phone number used for the transfer

- A description of what happened

- Any messages or emails related to the payment

Your bank might try to stop the transfer if it hasn’t been completed yet, such as when the recipient hasn't yet enrolled on Zelle. The bank might also open an investigation to determine whether the transaction qualifies for reimbursement under its policies.

Report the transaction and save evidence

In addition to contacting your bank, report the incident to the relevant authorities to protect others.

Steps to take include:

- File a report with the Federal Trade Commission (FTC) at reportfraud.ftc.gov. The FTC collects data on fraud and scams and uses reports to identify patterns and take action against bad actors.

- Contact the FBI’s Internet Crime Complaint Center (IC3) at ic3.gov if the scam involved online communication.

- Save all evidence related to the transaction. This includes screenshots of any messages, emails, or notifications connected to the scam, the transaction confirmation from your bank or Zelle, and any contact details associated with the person who received the funds.

What you can and cannot recover

Recovery of funds sent through Zelle depends largely on the circumstances of the transaction and your bank's specific policies. In general, banks may treat authorized payments differently from unauthorized ones. Here’s a breakdown of what to expect in different scenarios:

| Scenario | Can you recover the money? | What happens / why |

| Sent money to the wrong person (already enrolled in Zelle) | ❌ No | Recovery depends on the recipient voluntarily returning the money. |

| Pending payment to someone not yet registered | ✅ Possibly | You can cancel the payment if the recipient hasn’t enrolled yet. Once they enroll, the money is deposited automatically. |

| Authorized payment to a scammer (you approved it) | ❌ No | Usually not, but some impostor scams may qualify depending on the circumstances and your bank’s review. |

| Unauthorized transaction (account takeover) | ✅ Yes | If someone accessed your account without permission, the bank may investigate it as an unauthorized transaction under Regulation E (Electronic Fund Transfer Act). This means you’re more likely to be eligible for a refund under your bank's fraud protection policies. |

| Payment to a legitimate business gone wrong (no delivery, poor service) | ❌ No | Zelle doesn’t offer buyer protection or dispute resolution like credit cards or PayPal. |

| Sent money to a fake seller or marketplace scammer | ❌ No | Once sent, funds can’t be reversed. Recovery depends on the scammer (which is unlikely). |

| Duplicate payment (accidentally sent twice) | ❌ No | You’ll need to request a refund from the recipient. Zelle can’t reverse completed transfers. |

The broader takeaway is that Zelle offers limited recourse once a payment is made, which is why the habits for using Zelle safely matter.

FAQ: Common questions about staying safe on Zelle

Does Zelle have buyer protection?

For transactions where buyer protection matters, a credit card or a payment platform that includes purchase protection is a more suitable option.

Can someone hack your Zelle account?

Is Zelle safer than using a debit card?

Can banks reverse a Zelle payment?

Why do scammers prefer Zelle?

Should you use Zelle for Facebook Marketplace purchases?

If you do use Zelle for a marketplace purchase, only do so with someone whose identity you've verified and where the transaction is taking place in person.

Take the first step to protect yourself online. Try ExpressVPN risk-free.

Get ExpressVPN