The safest ways to pay online: Ultimate guide to the safest online payment methods

Not every payment method offers the same protection if something goes wrong.

Payment safety depends on these factors: reversibility, liability, and data exposure. These determine whether you can undo a payment, who absorbs the loss if fraud occurs, and how much of your financial data the seller receives.

Note: The information provided in this article is for general educational purposes only and should not be read as financial or legal advice.

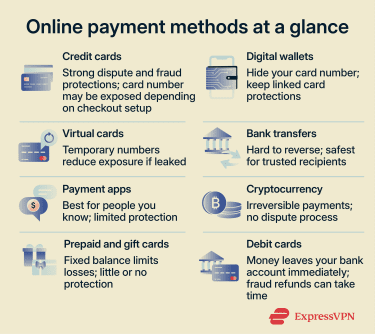

Online payment methods compared

The safest payment methods give you a way to dispute transactions and limit potential losses while reducing the amount of sensitive financial data exposed during checkout. Credit cards, digital wallets, and virtual cards offer this combination more consistently than other options.

Credit cards for online purchases

Credit cards include chargebacks and liability limits that many other payment methods lack. In the U.S., federal law limits liability for unauthorized credit card use to $50, while the Fair Credit Billing Act (FCBA) gives consumers a process for disputing billing errors, usually within 60 days after the first statement showing the error is sent. In the U.K., Section 75 of the Consumer Credit Act allows cardholders to claim against the credit card provider for purchases over £100 and up to £30,000 if something goes wrong. Many countries have comparable consumer protection frameworks, though the details vary.

Many major card networks and issuers go further with voluntary zero-liability policies. That means you usually don’t pay anything for unauthorized charges, even though the law would allow up to $50. These policies are set by issuers, not required by law.

A chargeback lets you dispute a charge through your card issuer and request a reversal, though approval isn’t guaranteed. You can file one for unauthorized transactions, goods that never arrived, or items significantly different from what was described. The issuer investigates and decides whether to reverse it. But the outcomes aren’t guaranteed. The process can take weeks, and the issuer may side with the merchant.

A card number alone often isn’t enough to complete the purchase. Some credit card payments include 3-D Secure, an extra identity check during checkout. You may be asked to enter a one-time passcode, approve the payment in your bank’s app, or confirm with your fingerprint. If the check is successfully completed, fraud liability for that transaction may shift from the merchant to the card issuer, depending on the card network’s rules.

When you enter your card number at checkout, the merchant may receive the full number, depending on how the payment is processed. This is known as the primary account number (PAN). Depending on how the payment is set up, the full card number may be retained to support refunds, repeat purchases, or subscriptions, or it may not be stored at all.

If the merchant’s systems are breached, attackers may obtain those details. Other payment methods (like digital wallets or virtual cards) can reduce this exposure.

Related: How to spot a credit card skimmer

Digital wallets for secure checkout

Apple Pay, Google Pay, and Samsung Pay use tokenization to help protect your card details. When you add a supported card, your bank, card issuer, payment network, or an authorized token service provider provisions a token or virtual card number for use with the wallet. This token replaces your actual card number during payment.

At checkout, the merchant typically receives the token or virtual card number, not your real card number. Wallet transactions may also include a transaction-specific security code or cryptogram that helps verify the payment came from the authorized device.

If a merchant is later breached, tokenization can reduce the impact because the merchant generally doesn’t store your actual card number. A stolen payment token is also less useful than a real card number because tokens are usually limited to a specific device, merchant, or payment scenario, and wallet transactions may require a fresh security code.

Tokenization is different from encryption. Encryption protects data by scrambling it so it can be read only by authorized parties. Tokenization replaces the card number with a substitute value, so the merchant can process the payment without receiving the actual card number.

Most mobile wallets also require device authentication, such as a fingerprint, facial recognition, or passcode, before approving payment. And since wallet payments are usually funded by a linked credit or debit card, the transaction generally keeps the protections associated with that card, including fraud protections and dispute rights, though the exact protections depend on the card type, country, issuer, and transaction.

Related: How to spot and prevent Apple Pay scams

Virtual cards for extra protection

Virtual cards are temporary card numbers generated by your bank or a payment service. They link to your real card but use a different card number and card verification value (CVV) for transactions. Some expire after one purchase. Others are locked to a specific merchant or subscription.

If a virtual card number is compromised, the exposure is limited to that number. Your actual card details aren’t shared with the merchant. You can cancel or replace the virtual card without affecting other payments.

Single-use cards work well for one-time purchases from unfamiliar sellers. Merchant-locked cards are better for subscriptions. Virtual cards may also include controls like spend limits or expiration dates, though availability varies by region.

It’s worth keeping in mind that virtual cards can complicate refunds if the card expires before the refund is processed. Before requesting a refund, check with your bank or card provider to confirm whether the money can still be returned to the expired virtual card or whether another process is required.

Bank transfers and ACH payments

Bank transfers move money directly between bank accounts. In the U.S., Automated Clearing House (ACH) payments handle direct deposits, bill payments, and account-to-account transfers. Wire transfers use a separate network and typically settle faster, especially for large payments.

These payments are harder to reverse than card transactions. Wire transfers are usually treated as final once processed. ACH payments are processed in batches and allow limited dispute resolution, such as for unauthorized transfers.

Bank transfers also share your bank account number and routing details with the recipient. These details can be used to initiate ACH debit requests that withdraw money from your account, though banks may apply authorization and fraud detection controls. Banks typically allow disputes for unauthorized debits, but you may need to contact your bank to block future withdrawals.

It’s important to distinguish between unauthorized transactions (fraud) and authorized payments that turn out to be scams. If you approve a transfer yourself, recovery is often much more difficult.

These methods are best used for payments to trusted recipients, such as a landlord, utility provider, or payroll system. Because reversals are limited, scammers often request bank transfers instead of payment methods that offer stronger dispute protections.

Payment apps for sending money

Venmo, Cash App, and Zelle are designed for peer-to-peer (P2P) transfers. Payments are typically fast and difficult to reverse once sent. These apps are best used for people you know, such as splitting a bill, repaying a friend, or sending money to family.

Zelle transfers money directly between bank accounts and doesn’t offer built-in purchase protection for goods or services.

Some payment apps offer limited protections when used for purchases. For instance, PayPal offers Purchase Protection when you select goods and services. Buyers can file disputes for items that don’t arrive or don’t match the description.

Because dispute options are limited compared to credit cards, these apps carry more risk when paying unfamiliar sellers. If something goes wrong, recovering the money may depend on the recipient voluntarily returning it.

Cryptocurrencies for online payments

Cryptocurrency payments are recorded on a blockchain, a public ledger shared across a distributed network. Once a transaction is confirmed, it generally can’t be reversed without the recipient’s cooperation. There's no bank or card issuer that can cancel the payment, and no chargeback process if something goes wrong.

Crypto payments don't require you to share your name, card number, or bank details with the seller. Instead, you send funds from one wallet address to another. These addresses don't directly identify you, but all transactions are publicly visible on the blockchain. If a wallet address is later linked to a person or service, past transactions tied to that address can also be associated with them.

Crypto can reduce the amount of personal information shared with a seller, but it also removes dispute options. If the seller doesn't deliver, recovering the payment is generally not possible.

Read more: Fake crypto wallets: How to identify and avoid the latest scams

Prepaid and gift cards

Prepaid and gift cards hold a fixed balance that isn’t tied directly to your primary bank account. If the card details are compromised, the potential loss is limited to the remaining balance.

These cards typically don’t include the same dispute rights as credit cards. Some prepaid cards may allow limited disputes, but protections vary by issuer. If a seller doesn’t deliver, recovering the funds can be difficult.

Gift cards are frequently requested in scam scenarios because the value can be transferred quickly once the code is shared. After redemption, recovery is usually not possible. Legitimate businesses and government agencies don’t request payment using gift cards.

Debit cards

Debit cards look and work like credit cards at checkout, but the money comes directly from your bank account.

With a credit card, the consumer doesn’t have to pay the disputed amount while the issuer investigates. Your available cash stays the same. With a debit card, the money is debited from your account immediately. You may not get it back until the bank completes its review of the claim. That review can take days or weeks. In the meantime, rent, bills, and everyday purchases can bounce or fail.

The legal protections are also narrower. In the U.S., the Electronic Fund Transfer Act (EFTA) sets liability at:

- $50 if you report within two business days.

- Up to $500 if you report within 60 days.

- Potentially unlimited after 60 days.

If you use a debit card online, linking it to a digital wallet adds tokenization and biometric authentication without changing the funding source. Your card number stays off the merchant's servers, even though the money still comes from your bank account.

Common online payment risks

Online payment scams usually aim to get you to approve a transaction or enter your payment details on a fake page.

Phishing scams often use emails, texts, or messages that impersonate banks, retailers, or payment providers. These messages link to fake websites designed to collect login credentials or payment details. The pages often copy the branding and layout of legitimate services. Information entered on the page is sent to the attacker.

Phishing messages typically claim an urgent problem, such as a failed payment, a suspicious login, or an expiring account. They direct the recipient to a page that may use a misspelled domain or an unfamiliar URL structure. The goal is to create enough urgency that the recipient acts before verifying.

Some rely on direct interaction, such as phone calls, messages, or marketplace conversations. The attacker may pose as a bank representative, seller, or customer support agent and claim that immediate payment or a transfer is required.

These scams rely on real-time interaction. The attacker adapts their story based on the target's responses. Legitimate banks and payment platforms don’t ask customers to transfer funds to protect an account.

Fraudulent stores and triangulation fraud schemes use steep discounts to attract buyers, collect payment, and either never ship the product or send a counterfeit. These sites often use professional product photos stolen from legitimate retailers, fabricated reviews, and functional checkout pages.

Prices significantly below typical retail can indicate a fraudulent listing, particularly when the same deal isn't available from established sellers. Some of these storefronts operate briefly before being taken down and reappearing under a different domain.

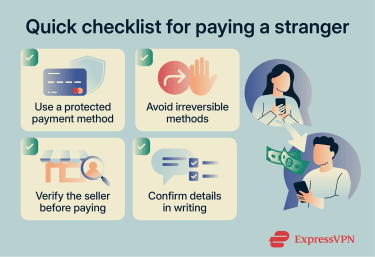

How to safely pay a stranger online

Buying from an individual or an unfamiliar seller carries more risk than purchasing from an established retailer. There's typically no return policy, no customer service, and limited ways to verify the seller's identity.

Choose a method with buyer protection

PayPal's "goods and services" option and credit cards both allow buyers to file disputes if a transaction goes wrong. If the platform offers its own protected checkout (such as eBay's managed payments), that's generally the safer option because disputes are handled within the platform. Moving a transaction off-platform can remove these protections, making it harder to recover your money if something goes wrong.

Avoid irreversible payment types

Bank transfers, Zelle, cryptocurrency, gift cards, and P2P apps offer limited or no dispute options. Paying with any of these reduces your ability to recover funds if the seller doesn't deliver.

Confirm the seller and transaction details

On marketplace platforms, check the seller's history, ratings, and reviews. On external platforms, reverse-image search product photos to check whether they've been copied from another listing. Confirm the exact item, price, and shipping terms in writing before sending payment.

FAQ: Common questions about the safest online payment methods

Which online payment method offers the best buyer protection?

Are digital wallets safer than using a card directly?

When should I use a virtual card for online payments?

Are bank transfers ever safe for online payments?

How do chargebacks help protect online purchases?

What signs show that an online checkout page is secure?

Explore the web with greater privacy

Get ExpressVPNSign up today for a chance to win FIFA World Cup 2026™ tickets.

Comments

Great article on online payment safety! It offers valuable insights into choosing the most secure methods for protecting your transactions.