Expressvpn Glossary

Payment Card Industry Data Security Standard

What is the Payment Card Industry Data Security Standard (PCI DSS)?

The Payment Card Industry Data Security Standard (PCI DSS) was developed by the PCI Security Standards Council and sets security requirements for organizations that handle cardholder data. It covers any organization that stores, processes, or transmits cardholder data.

PCI DSS is an industry standard, not a law, but payment brands and acquiring banks require compliance to process card payments. Non-compliance can result in fines or restrictions.

How does PCI DSS work?

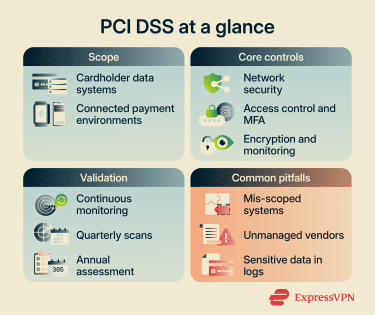

PCI DSS sets 12 core security requirements designed to protect cardholder data. These requirements apply to systems within the cardholder data environment, including connected systems that could affect payment security.

Organizations define the cardholder data environment, apply required controls, and validate them through assessments and scans.

The 12 requirements are grouped into six control objectives:

- Network security: Maintain secure networks and configurations.

- Protecting cardholder data: Encrypt and limit storage of card data.

- Vulnerability management: Patch systems and use security tools.

- Access control: Restrict access and enforce strong authentication.

- Monitoring and testing: Log activity and test controls regularly.

- Security policies: Maintain and enforce security processes.

PCI DSS requires ongoing monitoring, testing, and maintenance rather than one-time certification.

Where is PCI DSS used?

PCI DSS applies to any environment where a business handles cardholder data. This can include:

- E-commerce and payment gateways (for example, online checkouts and hosted payment pages).

- Point-of-sale (POS) systems (for example, in-store card terminals).

- Call centers (for example, phone payments handled by agents).

- Cloud environments (for example, systems that store or process payment data).

- Third-party service providers (for example, payment processors and hosting providers).

- Financial institutions (for example, issuing and acquiring banks).

Types of PCI DSS compliance validation

PCI DSS validation requirements depend on the type of organization and the number of card transactions it processes each year. Card brands such as Visa and Mastercard group organizations into levels based on transaction volume. These levels determine how each organization must review and report its compliance.

Service providers often face stricter validation requirements than merchants, especially when they process large volumes of cardholder data or support multiple payment clients.

Common validation methods include:

- Self-assessment questionnaires (SAQs): Eligible merchants complete a questionnaire to confirm that required security controls are in place. Eligibility depends on how the merchant handles and processes cardholder data.

- On-site audits: Larger merchants and many service providers undergo an assessment conducted by a Qualified Security Assessor (QSA). This review results in a Report on Compliance.

- Attestation of compliance (AOC): After completing a questionnaire or audit, organizations submit a formal statement confirming their compliance status.

- Approved vulnerability scans: Some organizations must complete regular external scans performed by an Approved Scanning Vendor (ASV).

Why is PCI DSS important?

PCI DSS provides a standardized framework for protecting cardholder data and securing payment environments. It helps reduce the risk of data exposure and supports trust between businesses, payment networks, and customers.

Compliance is typically required to process card payments and maintain relationships with acquiring banks.

Some of the most common benefits of PCI DSS compliance include:

- Standardized security controls: More consistent protection across systems.

- Improved incident readiness: Faster detection and response.

- Stronger vendor oversight: Clearer expectations for third parties.

- Safer outsourcing: Better control over external payment partners.

- Broader compliance alignment: Less overlap across security efforts.

Risks and privacy concerns of PCI DSS

PCI DSS can strengthen payment security, but gaps in implementation or oversight can introduce new risks, such as:

- Mis-scoped systems: Some systems may fall outside protection.

- Expanded third-party scope: Vendor use increases oversight complexity.

- Sensitive data in logs: Logging may capture more data than intended.

- Checklist-driven compliance: Minimum focus can miss broader risks.

- Weak network segmentation: Poor separation increases breach impact.

Further reading

- Credit card authorization: The complete guide you need

- Ultimate guide to the safest online payment methods

- Online shopping safety tips: Protect yourself from scams

- Complete guide to Apple’s mobile payment security